The closure of the Strait of Hormuz in 2026 creates a fundamental disruption that affects both global energy systems and international financial networks. The maritime chokepoint exists as a narrow waterway which connects the Iranian coast to the Musandam Peninsula of Oman and it handles daily oil and petroleum product shipments that range from 20 million to 21 million barrels which represent 20 percent to 25 percent of worldwide maritime oil and petroleum product transportation.

The 2026 Iran-U.S.-Israel conflict reached its peak when both sides implemented a complete maritime blockade which cut off this essential energy supply route and created the most extensive supply interruption ever recorded in the global oil market. This study investigates the events which created the crisis and the operational methods used in the blockade and the major consequences which reshaped international power structures through changes in currency dominance and petroleum distribution and natural gas transportation systems.

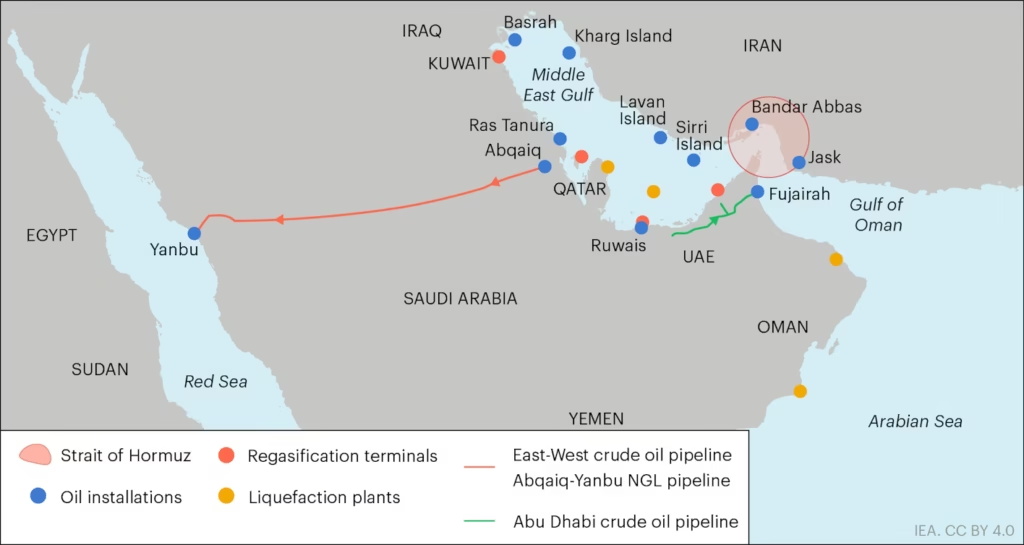

The Strategic Imperative of the Strait of Hormuz

The 2026 crisis develops from the geographic and technical limitations which exist within the Strait of Hormuz. The strait at its narrowest point measures 29 nautical miles yet contains two 2-mile-wide shipping lanes which navigators can use between a 2-mile buffer zone. The physical narrowness of the area enables even small military or asymmetric forces to achieve strong control over international trade activities. The strait has functioned as the main export pathway for Saudi Arabia, the United Arab Emirates (UAE), Kuwait, Qatar, Iraq, Bahrain, and Iran throughout its history.

The existing export routes provide some alternative options, but they cannot match the total export capacity which would result from complete closure of the strait. Saudi Arabia operates the East-West pipeline to the Red Sea, and the UAE maintains a pipeline to the port of Fujairah, but these alternatives together offer only 3.5 million to 5.5 million barrels per day of bypass capacity. The complete blockade situation results in the shutdown of more than 15 million barrels which represent daily crude production together with almost 5 million barrels of refined product exports. The structural weakness creates an “economic clock of war” which functions because the blockade length establishes whether its effects will cause localized price increases or result in worldwide economic growth combined with inflationary turmoil.

Sequence of Events: The Road to the 2026 Blockade

The 2026 crisis started because existing regional tensions reached a new level of escalation. The US and Israeli military forces conducted coordinated airstrikes against major Iranian nuclear sites on February 28 2026 after the US received intelligence that Iran would achieve its enrichment program goals.

The initial airstrikes created global market instability which resulted in Brent crude oil prices increasing 6% within one day because traders expected the strait to be closed in retaliation.

The maritime environment started to show signs of deterioration on March 1 2026 when commercial tankers began to leave their routes because security conditions became more dangerous. Many crude oil and liquefied natural gas (LNG) ships maintained their positions outside the strait because they wanted to protect themselves after insurers started to change their assessment of war-risk coverage. The Iranian parliament conducted its first official session about the closure on March 4 2026 while the Iranian military established a complete border blockade. Tehran declared that navigation would proceed only “according to measures which result from the state of belligerency” which enabled them to control access to the waterway.

The crisis reached a higher level of intensity during March and April because diplomatic attempts to find a solution proved unsuccessful. The “Islamabad Talks” which took place on April 11 and 12 2026 lasted for 21 hours but ended without reaching an agreement because both sides stayed stuck in negotiations about the Iranian nuclear program and Iranian transit tolls.

(via Getty Images)

After the US President Donald Trump announced a naval blockade against Iranian ports on April 13 2026 the US Navy received orders to stop all ships from entering or leaving Iranian waters while also removing sea mines that Iranian forces had placed.

The Mechanics of Asymmetric Maritime Warfare

Iranian forces used multiple defence layers which included sea mines and drone swarms and fast-attack boats to stop all maritime operations.

Iran used small boat swarm tactics which they had developed since the late 1980s to send 20 to 50 fast-attack boats which carried anti-ship missiles and rockets to strike commercial vessels. The manoeuvres resulted in total vessel traffic disruption which continued until early April when daily transits dropped from 138 to 16 ships per day.

The mine threat proved to be a major disruptive force. Sea mines establish permanent “area denial” zones which require dedicated mine-hunting vessels to perform their functions unlike standard naval equipment. Analysts estimated that clearing the strait would require 12 to 15 specialized ships, 6 to 8 destroyers for escort, and continuous air cover, a process likely to last months rather than weeks. The operational environment established a “soft closure” of navigation despite boats being able to pass through the area because shipowners chose to protect their assets in unsafe waters.

The Petroleum Shock and Global Market Fragmentation

The blockade brought about its first result which created a supply interruption that removed almost 20 percent of global petroleum liquids from the market. The oil market experienced price increases as Brent crude reached a peak of $120 per barrel before entering a fluctuating period between $90 and $110. The physical markets experienced their highest impact when Asian buyers had to pay $20 to $25 above Brent financial benchmarks to acquire the last available spot cargoes.

The energy market crisis created two separate systems which operated independently from each other: the Gulf-based system which had stranding and supply shortages and the Atlantic Basin system which maintained its delivery capabilities. The Western Hemisphere producers from the United States and Canada and Brazil and Guyana obtained financial benefits from higher prices while avoiding the Hormuz chokepoint operational dangers. Asian nations experienced major fuel shortages which led to fuel rationing because they require 75% to 80% of the oil that passes through the strait.

The shock affected all refined products which included diesel gasoline and jet fuel. The global refinery margins faced extreme changes because of increased feedstock prices and interrupted shipping operations while airlines had to end flights or increase their ticket costs to sustain their financial operations. The average gasoline price in the United States reached $4 per gallon which created domestic inflation and decreased the ability of households to spend money.

The LNG Crisis and European Energy Vulnerability

While oil received substantial attention, the interruption of liquefied natural gas (LNG) shipments created equal damage to international energy security. The Strait of Hormuz serves as the essential shipping route which enables Qatar and UAE to export their LNG supplies, which together account for about 20 percent of the worldwide LNG market. The global gas market experienced a major supply loss when QatarEnergy announced force majeure on its exports because the blockade caused gas prices to almost double in Asia and Europe.

This “second energy crisis” hit Europe particularly hard. After Russia stopped supplying gas through pipelines in 2022, European countries relied on Qatari LNG to protect themselves from supply disruptions. European power companies needed to buy American and West African cargoes through costly spot-market bidding because the 2026 blockade demonstrated the strategy’s limitations. Dutch TTF gas benchmarks reached more than €60/MWh, which caused manufacturing in the European Union to decline because companies had to pay additional fees that reached 30 percent for electricity and feedstock.

The LNG shock presents greater challenges for resolution than the oil shock because LNG systems lack the bypass pipeline networks which exist for crude oil transportation. This “geopolitical tripwire” creates a direct connection between Gulf military conflicts and the costs which Asian and European utilities and industrial businesses and importers must pay. The resulting price instability has required energy networks to change their structures because Europe now depends more on American energy supplies while it attempts to achieve strategic independence.

The Erosion of the Petrodollar and the Financial Shift

The 2026 crisis which triggered the downfall of the petrodollar system established in 1970s has continued to destroy American economic supremacy. The global oil market has used U.S. dollars as its standard currency for several decades which creates ongoing demand for dollars and enables the United States to fund its budget deficits through international purchases of Treasury bonds. The 2026 conflict revealed the strategic dangers which stem from this dependence.

Through its control of the strait Iran used the strait to dispute the dollar’s established dominance. Tehran announced to countries that safe passage through the strait or oil purchases required payment in Chinese Yuan or other non-dollar currencies which he used to reject the dollar’s exclusive use in energy transactions. Reports indicate that tankers paid for their passage using yuan-based tolls while negotiations to receive oil-linked payments in yuan reveal the establishment of a separate petroyuan market system.

BRICS nations have started to de-dollarize through this change which now includes Saudi Arabia and the UAE as major oil-producing countries. The countries have increasingly preferred to use their domestic currencies for trade settlements because this practice minimizes their risk of encountering Western financial sanctions and dollar-based economic restrictions. The dollar pegs and U.S. Treasury holdings of Gulf states need to end because this would decrease dollar demand which forces U.S. borrowing costs to rise while undermining the dollar’s position as the primary global reserve currency.

Project mBridge and the Digital Currency Frontier

The new digital financial infrastructure which includes Project mBridge enables the petroyuan to achieve its increasing popularity. The multi-central bank digital currency (multi-CBDC) platform unites the central banks from mainland China, Hong Kong, Thailand, the UAE, and Saudi Arabia.

The platform reached a transaction volume of over $55 billion through 4,000 cross-border transactions by late 2025, which represents a 2,500-time increase from its 2022 pilot phase. The digital yuan (e-CNY) accounts for approximately 95% of the settlement volume on mBridge.

The platform established direct trade settlement during the 2026 crisis, which eliminated the requirement for conventional correspondent banking and the U.S.-run SWIFT system. Sanctioned countries like Iran now have the ability to use intermediaries or digital conduits for dollar-denominated transactions, which enables them to bypass dollar-denominated systems. The People’s Bank of China changed the e-CNY from a “digital cash” tool to a “digital deposit currency” in early 2026, which allows banks to use it for asset and liability management while its international trade and value storage functions continue to grow.

Experts disagree about whether the U.S. dollar will continue to dominate because American financial markets provide unmatched liquidity, but Project mBridge and the digital yuan create alternate payment systems, which reduce American financial dominance in selected energy and commodity regions. The multipolar financial order establishes a system which limits the power of Western countries to impose unilateral financial penalties, while allowing oil-producing countries to maintain financial freedom.

Geopolitical Realignment: Winners and Losers

The international political landscape has completely transformed after the 2026 Hormuz crisis. The United States maintains its position as a strong energy producer because international demand for its energy products has increased while its energy prices have risen. The military force of the United States has failed to maintain its status as a security provider because it has not restored commercial shipping through the strait. The Gulf security umbrella of the United States has started to weaken which results in rising domestic political pressures while the country faces increased borrowing costs.

Russia has become the main indirect winner from these events. Russian fossil fuel revenues reached their lowest point of approximately $501 million per day in early 2026 but Western sanctions failed to stop their growth because Russia supplied Asian markets with energy. The Atlantic Basin exporters including Norway Brazil and Canada have experienced price increases while their shipping operations have remained operational because Gulf exporters faced operational delays.

The Gulf Cooperation Council (GCC) monarchies currently deal with a fundamental danger that threatens their entire economic system. The revenue loss from the blockade occurs at a critical period because some states face double-digit economic contractions. The Gulf area lost its reputation as a secure investment zone because of the conflict which forced countries to change their security partnerships while seeking new import routes that bypass Iranian-controlled waterways.

Implications for India: Strategic vulnerability and opportunity

The Hormuz crisis demonstrates to India which energy threat affects their ability to protect their economic growth. The situation raises multiple urgent inquiries. Should India aggressively diversify its import routes? What is the maximum rate at which India can build its strategic petroleum reserves? What responsibilities does the Indian Navy need to assume for protecting these dangerous maritime routes? The need for this energy transition might drive India towards renewable energy sources while creating new pathways through the INSTC. The persistent conflicts in this region seem to fuel India’s development of its most effective long-term strategic approach.